Model Training and Tuning

Contents

- Baseline Models

- Feature Engineering Attempts

- Decision Tree Model Tuning/Comparison

- Random Forest Model Tuning/Comparison

- Comparison of Top Decision Tree vs. Top Random Forest Models

When building and testing models for real-world use, we should choose model performance metrics based on the goal and usage of the model. In our case, we will be focusing on a high precision bar where the positive outcome is a fully paid off loan and then maximizing the total number of true positives.

We have chosen to limit ourselves to decision tree-based algorithms because they are flexible and apply to broad types of data. We have some important ordinal variables in our dataset, including loan subgrade.

Imports and Loading Data

import requests

from IPython.core.display import HTML

styles = requests.get("https://raw.githubusercontent.com/Harvard-IACS/2018-CS109A/master/content/styles/cs109.css").text

HTML(styles)

from IPython.display import clear_output

from datetime import datetime

from sklearn.linear_model import LinearRegression

from sklearn.linear_model import LogisticRegressionCV

from sklearn.neighbors import KNeighborsRegressor

from sklearn.tree import DecisionTreeClassifier

from sklearn.ensemble import RandomForestClassifier

from sklearn.metrics import accuracy_score, recall_score, precision_score, balanced_accuracy_score

from sklearn.model_selection import cross_val_score, train_test_split

from sklearn.metrics import confusion_matrix, classification_report

%matplotlib inline

import numpy as np

import pandas as pd

import matplotlib

import matplotlib.pyplot as plt

import seaborn as sns

sns.set(font_scale=1.5)

sns.set_style('ticks')

from os import listdir

from os.path import isfile, join

import warnings

warnings.filterwarnings('ignore')

import os

#Google Collab Only

from google.colab import drive

drive.mount('/content/gdrive', force_remount=False)

clean_df = pd.read_pickle('/content/gdrive/My Drive/Lending Club Project/data/Pickle/clean_df_Mon.pkl').sample(frac=.10, random_state=0)

#clean_df = pd.read_pickle('./data/Pickle/clean_df.pkl').sample(frac=.10, random_state=0)

print(clean_df.shape)

outcome='fully_paid'

data_train, data_val = train_test_split(clean_df, test_size=.1, stratify=clean_df[outcome], random_state=99);

X_train = data_train.drop(columns=['issue_d', 'zip_code', 'addr_state', outcome])

y_train = data_train[outcome]

X_val = data_val.drop(columns=['issue_d', 'zip_code', 'addr_state', outcome])

y_val = data_val[outcome]

(108744, 87)

Baseline Models

Since we have performed feature selection using Random Forest, we will use a single Decision Tree as our baseline with the top 15 features chosen by feature importances.

First, for comparison purposes, we compute an accuracy score from a trival model: a model in which we simply predict all loans to have the outcome of the most-common class (i.e., predicting all loans to be fully paid).

importances = ['int_rate', 'sub_grade', 'dti', 'installment', 'avg_cur_bal', 'credit_line_age', 'bc_open_to_buy', 'mo_sin_old_rev_tl_op', 'annual_inc', 'mo_sin_old_il_acct', 'tot_hi_cred_lim', 'revol_util', 'bc_util', 'revol_bal', 'tot_cur_bal', 'total_rev_hi_lim', 'total_bal_ex_mort', 'total_bc_limit', 'loan_amnt', 'total_il_high_credit_limit', 'grade', 'mths_since_recent_bc', 'total_acc', 'mo_sin_rcnt_rev_tl_op', 'num_rev_accts', 'num_il_tl', 'mths_since_recent_inq', 'mo_sin_rcnt_tl', 'num_bc_tl', 'acc_open_past_24mths', 'num_sats', 'open_acc', 'pct_tl_nvr_dlq', 'num_op_rev_tl', 'mths_since_last_delinq', 'percent_bc_gt_75', 'num_rev_tl_bal_gt_0', 'num_actv_rev_tl', 'num_bc_sats', 'num_tl_op_past_12m', 'term_ 60 months', 'num_actv_bc_tl', 'mths_since_recent_revol_delinq', 'mort_acc', 'mths_since_last_major_derog', 'tot_coll_amt', 'mths_since_recent_bc_dlq', 'mths_since_last_record', 'inq_last_6mths', 'num_accts_ever_120_pd', 'delinq_2yrs', 'pub_rec', 'verification_status_Verified', 'verification_status_Source Verified', 'emp_length_10+ years', 'purpose_debt_consolidation', 'emp_length_5-9 years', 'emp_length_2-4 years', 'home_ownership_RENT', 'home_ownership_MORTGAGE', 'purpose_credit_card', 'pub_rec_bankruptcies', 'home_ownership_OWN', 'num_tl_90g_dpd_24m', 'tax_liens', 'purpose_home_improvement', 'purpose_other', 'collections_12_mths_ex_med', 'purpose_major_purchase', 'purpose_small_business', 'purpose_medical', 'application_type_Joint App', 'purpose_moving', 'chargeoff_within_12_mths', 'delinq_amnt', 'purpose_vacation', 'purpose_house', 'acc_now_delinq', 'purpose_wedding', 'purpose_renewable_energy', 'home_ownership_OTHER', 'home_ownership_NONE', 'purpose_educational']

top_15_features = importances[:15]

**For the purposes of our baseline model, we simply select the top 15 features from the random forest feature importances. We train and compare decison trees using this subset of features. **

In subsequent models, we will engineer new features and carefully tune the subset of features to include.

most_common_class = data_train[outcome].value_counts().idxmax()

## training set baseline accuracy

baseline_accuracy = np.sum(data_train[outcome]==most_common_class)/len(data_train)

print("Classification accuracy (training set) if we predict all loans to be fully paid: {:.3f}"

.format(baseline_accuracy))

Classification accuracy (training set) if we predict all loans to be fully paid: 0.799

Now we train our baseline models on the subset of features. For baseline models we simply use the default DecisionTreeClassifier (which uses class_weights=None), trained on max_depths from 2 to 10.

We store various performance metrics; in addition to the accuracy score, we also store the balanced accuracy score, precision score, and confusion matrix for each model so that we can investigate beyond a simple accuracy score.

data_train_baseline = data_train[top_15_features+[outcome]]

data_val_baseline = data_val[top_15_features+[outcome]]

def compare_tree_models(data_train, data_val, outcome, class_weights=[None], max_depths=range(2,21)):

X_train = data_train.drop(columns=outcome)

y_train = data_train[outcome]

X_val = data_val.drop(columns=outcome)

y_val = data_val[outcome]

results_list = []

for class_weight in class_weights:

for depth in max_depths:

clf = DecisionTreeClassifier(criterion='gini', max_depth=depth, class_weight=class_weight)

clf.fit(X_train, y_train)

y_train_pred = clf.predict(X_train)

y_val_pred = clf.predict(X_val)

train_accuracy = accuracy_score(y_train, y_train_pred)

train_balanced_accuracy = balanced_accuracy_score(y_train, y_train_pred)

train_precision = precision_score(y_train, y_train_pred)

train_cm = confusion_matrix(y_train, y_train_pred)

val_accuracy = accuracy_score(y_val, y_val_pred)

val_balanced_accuracy = balanced_accuracy_score(y_val, y_val_pred)

val_precision = precision_score(y_val, y_val_pred)

val_cm = confusion_matrix(y_val, y_val_pred)

results_list.append({'Depth': depth,

'class_weight': class_weight,

'Train Accuracy': train_accuracy,

'Train Balanced Accuracy': train_balanced_accuracy,

'Train Precision': train_precision,

'Train CM': train_cm,

'Val Accuracy': val_accuracy,

'Val Balanced Accuracy': val_balanced_accuracy,

'Val Precision': val_precision,

'Val CM': val_cm})

columns=['Depth', 'class_weight', 'Train Accuracy', 'Train Balanced Accuracy',

'Train Precision', 'Val Accuracy', 'Val Balanced Accuracy', 'Val Precision']

results_table = pd.DataFrame(results_list, columns=columns)

return results_table, results_list

results_table, results_list = compare_tree_models(data_train_baseline, data_val_baseline, outcome='fully_paid')

results_table

| Depth | class_weight | Train Accuracy | Train Balanced Accuracy | Train Precision | Val Accuracy | Val Balanced Accuracy | Val Precision | |

|---|---|---|---|---|---|---|---|---|

| 0 | 2 | None | 0.799313 | 0.500000 | 0.799313 | 0.799356 | 0.500000 | 0.799356 |

| 1 | 3 | None | 0.799313 | 0.500000 | 0.799313 | 0.799356 | 0.500000 | 0.799356 |

| 2 | 4 | None | 0.799487 | 0.536238 | 0.811405 | 0.800828 | 0.539709 | 0.812626 |

| 3 | 5 | None | 0.801163 | 0.530861 | 0.809520 | 0.800276 | 0.532327 | 0.810081 |

| 4 | 6 | None | 0.801561 | 0.516372 | 0.804640 | 0.800276 | 0.516537 | 0.804748 |

| 5 | 7 | None | 0.802409 | 0.533414 | 0.810372 | 0.799632 | 0.531752 | 0.809895 |

| 6 | 8 | None | 0.804892 | 0.532469 | 0.810003 | 0.798529 | 0.527458 | 0.808444 |

| 7 | 9 | None | 0.807804 | 0.542317 | 0.813327 | 0.796046 | 0.528136 | 0.808716 |

| 8 | 10 | None | 0.812607 | 0.555445 | 0.817789 | 0.790437 | 0.526687 | 0.808306 |

| 9 | 11 | None | 0.818492 | 0.579222 | 0.826148 | 0.786943 | 0.532911 | 0.810540 |

| 10 | 12 | None | 0.825798 | 0.597175 | 0.832476 | 0.782805 | 0.534099 | 0.811045 |

| 11 | 13 | None | 0.834677 | 0.627171 | 0.843528 | 0.778943 | 0.542324 | 0.814104 |

| 12 | 14 | None | 0.845283 | 0.648505 | 0.851235 | 0.772598 | 0.536639 | 0.812186 |

| 13 | 15 | None | 0.856625 | 0.676915 | 0.861953 | 0.767816 | 0.542058 | 0.814309 |

| 14 | 16 | None | 0.869509 | 0.706900 | 0.873438 | 0.758989 | 0.540312 | 0.813896 |

| 15 | 17 | None | 0.882343 | 0.734165 | 0.883942 | 0.753839 | 0.540009 | 0.813922 |

| 16 | 18 | None | 0.895769 | 0.769274 | 0.898327 | 0.748046 | 0.543251 | 0.815341 |

| 17 | 19 | None | 0.908796 | 0.797957 | 0.910013 | 0.741517 | 0.540368 | 0.814411 |

| 18 | 20 | None | 0.920578 | 0.827289 | 0.922590 | 0.734069 | 0.541717 | 0.815169 |

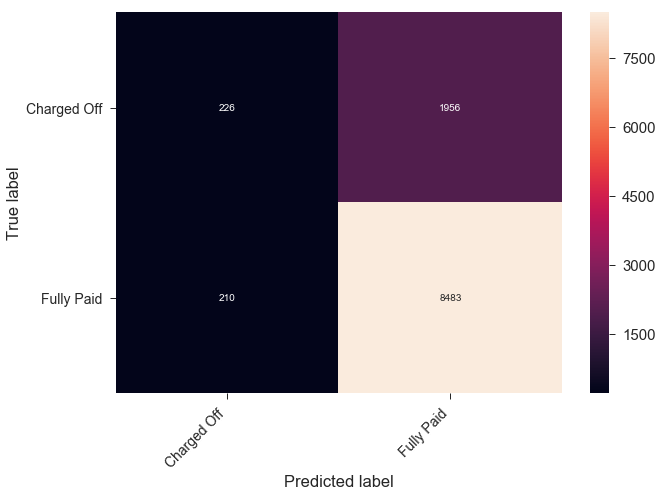

def print_confusion_matrix(confusion_matrix, class_names, figsize = (10,7), fontsize=14):

"""Prints a confusion matrix, as returned by sklearn.metrics.confusion_matrix, as a heatmap.

Arguments

---------

confusion_matrix: numpy.ndarray

The numpy.ndarray object returned from a call to sklearn.metrics.confusion_matrix.

Similarly constructed ndarrays can also be used.

class_names: list

An ordered list of class names, in the order they index the given confusion matrix.

figsize: tuple

A 2-long tuple, the first value determining the horizontal size of the ouputted figure,

the second determining the vertical size. Defaults to (10,7).

fontsize: int

Font size for axes labels. Defaults to 14.

Returns

-------

matplotlib.figure.Figure

The resulting confusion matrix figure

"""

df_cm = pd.DataFrame(

confusion_matrix, index=class_names, columns=class_names,

)

fig = plt.figure(figsize=figsize)

try:

heatmap = sns.heatmap(df_cm, annot=True, fmt="d")

except ValueError:

raise ValueError("Confusion matrix values must be integers.")

heatmap.yaxis.set_ticklabels(heatmap.yaxis.get_ticklabels(), rotation=0, ha='right', fontsize=fontsize)

heatmap.xaxis.set_ticklabels(heatmap.xaxis.get_ticklabels(), rotation=45, ha='right', fontsize=fontsize)

plt.ylabel('True label')

plt.xlabel('Predicted label')

return fig

best_model_index = results_table['Val Accuracy'].idxmax()

cm = results_list[best_model_index]['Val CM']

fig = print_confusion_matrix(cm, class_names=['Charged Off', 'Fully Paid'])

Comments: Our baseline accuracy values are not impressive; the best accuracy score on the validation set is about 80%, which is the accuracy we’d achieve if we simply predicted all loans to be fully paid.

Though we have used accuracy as the scoring metric for our baseline model, we realize that this is not the most appropriate metric to use going forward. We should also consider other performance metrics, such as precision scores and balanced accuracy scores.

Going forward, we should also place more weight (i.e., by modifyinng the class_weight when training models) on correctly classifying loans that are charged off. There are two main reasons for this:

- 80% of the loans in our dataset are, in fact, fully paid. We should add more weight to the charged-off loans to account for this imbalance in the loan outcome labels.

- For the purposes of building a sound, reasonably low-risk investment strategy, we hope to minimize the particular error in which the model predicts a loan to be fully paid when it is truly charged off. We will tune the class_weight parameter in future models to select an optimal value for our purposes.

Feature Engineering Attempts

To enhance model performance while tuning our models, , we explored generating additional features not in the raw data set to potentially catch additional relationships in the response variable.

Our attempts included interaction variables between top features, as well as polynomial terms with degree 2. Unfortunately, we did not see any notable model performance from these changes, so they were not included in our final model.

There are many other higher-order polynomial and interaction terms and combinations of relevant/related predictors that could also be fine-tuned into better summary variables to boost model performance. This feature engineering step is an area where there is room for substantial improvement upon our model in the future.

def sum_cols_to_new_feature(df, new_feature_name, cols_to_sum, drop=True):

new_df = df.copy()

new_df[new_feature_name] = 0

for col in cols_to_sum:

new_df[new_feature_name] = new_df[new_feature_name] + new_df[col]

if drop:

new_df = new_df.drop(columns=cols_to_sum)

return new_df

def add_interactions(loandf):

df = loandf.copy()

df['int_rate_X_sub_grade'] = df['int_rate']*df['sub_grade']

df['installment_X_sub_grade'] = df['installment']*df['sub_grade']

df['installment_X_int_rate'] = df['installment']*df['int_rate']

df['int_rate_X_sub_grade_X_installment'] = df['int_rate']*df['sub_grade']*df['installment']

df['dti_X_sub_grade'] = df['dti']*df['sub_grade']

df['mo_sin_old_rev_tl_op_X_sub_grade'] = df['mo_sin_old_rev_tl_op']*df['sub_grade']

df['dti_X_mo_sin_old_rev_tl_op_X_sub_grade'] = df['dti']*df['mo_sin_old_rev_tl_op']*df['sub_grade']

df['income_to_loan_amount'] = df['annual_inc']/df['loan_amnt']

df['dti_X_income'] = df['dti']*df['annual_inc']

df['dti_X_income_X_loan_amnt'] = df['annual_inc']*df['loan_amnt']*df['dti']

df['dti_X_loan_amnt'] = df['dti']*df['loan_amnt']

df['avg_cur_bal_X_dti'] = df['avg_cur_bal']*df['dti']

return df

outcome='fully_paid'

#clean_df = pd.read_pickle('./data/Pickle/clean_df.pkl').sample(frac=0.05, random_state=0)

clean_df = pd.read_pickle('/content/gdrive/My Drive/Lending Club Project/data/Pickle/clean_df_Mon.pkl').sample(frac=.05, random_state=0)

clean_df = add_interactions(clean_df)

clean_df = sum_cols_to_new_feature(clean_df, new_feature_name='months_since_delinq_combined',

cols_to_sum=['mths_since_last_delinq', 'mths_since_last_major_derog','mths_since_last_record',

'mths_since_recent_bc_dlq', 'mths_since_recent_revol_delinq'], drop=True)

clean_df = sum_cols_to_new_feature(clean_df, new_feature_name='num_bad_records',

cols_to_sum=['num_accts_ever_120_pd','num_tl_90g_dpd_24m','pub_rec',

'pub_rec_bankruptcies', 'tax_liens'], drop=True)

clean_df = sum_cols_to_new_feature(clean_df, new_feature_name='combined_credit_lim',

cols_to_sum=['tot_hi_cred_lim','total_bc_limit','total_il_high_credit_limit',

'total_rev_hi_lim',], drop=True)

clean_df = sum_cols_to_new_feature(clean_df, new_feature_name='num_recent_delinq',

cols_to_sum=['delinq_2yrs', 'chargeoff_within_12_mths', 'collections_12_mths_ex_med'], drop=True)

clean_df = sum_cols_to_new_feature(clean_df, new_feature_name='num_accounts',

cols_to_sum=['num_bc_tl', 'num_il_tl', 'num_op_rev_tl', 'num_rev_accts',

'num_actv_rev_tl', 'num_actv_bc_tl', 'mort_acc'], drop=True)

clean_df = clean_df.drop(columns = ['issue_d', 'zip_code', 'addr_state'])

data_train, data_test = train_test_split(clean_df, test_size=.1, stratify=clean_df[outcome], random_state=99);

X_train = data_train.drop(columns=outcome)

y_train = data_train[outcome]

rf_model = RandomForestClassifier(n_estimators=50, max_depth=50).fit(X_train, y_train)

importances = pd.DataFrame({'Columns':X_train.columns,'Feature_Importances':rf_model.feature_importances_})

importances = importances.sort_values(by='Feature_Importances',ascending=False)

print(importances['Columns'].values.tolist()[:15])

['dti_X_sub_grade', 'int_rate', 'int_rate_X_sub_grade_X_installment', 'int_rate_X_sub_grade', 'dti_X_mo_sin_old_rev_tl_op_X_sub_grade', 'dti', 'income_to_loan_amount', 'avg_cur_bal', 'dti_X_loan_amnt', 'mo_sin_old_il_acct', 'mo_sin_old_rev_tl_op_X_sub_grade', 'bc_open_to_buy', 'installment_X_sub_grade', 'sub_grade', 'revol_bal']

def compare_tree_models(data_train, data_val, outcome, class_weights=[None], max_depths=range(2,21)):

X_train = data_train.drop(columns=outcome)

y_train = data_train[outcome]

X_val = data_val.drop(columns=outcome)

y_val = data_val[outcome]

tree_results = []

for class_weight in class_weights:

for depth in max_depths:

clf = DecisionTreeClassifier(criterion='gini', max_depth=depth, class_weight=class_weight)

clf.fit(X_train, y_train)

y_train_pred = clf.predict(X_train)

y_val_pred = clf.predict(X_val)

train_accuracy = accuracy_score(y_train, y_train_pred)

train_balanced_accuracy = balanced_accuracy_score(y_train, y_train_pred)

train_precision = precision_score(y_train, y_train_pred)

train_cm = confusion_matrix(y_train, y_train_pred)

val_accuracy = accuracy_score(y_val, y_val_pred)

val_balanced_accuracy = balanced_accuracy_score(y_val, y_val_pred)

val_precision = precision_score(y_val, y_val_pred)

val_cm = confusion_matrix(y_val, y_val_pred)

tree_results.append({'Depth': depth,

'class_weight': class_weight,

'Train Accuracy': train_accuracy,

'Train Balanced Accuracy': train_balanced_accuracy,

'Train Precision': train_precision,

'Train CM': train_cm,

'Val Accuracy': val_accuracy,

'Val Balanced Accuracy': val_balanced_accuracy,

'Val Precision': val_precision,

'Val CM': val_cm})

return tree_results

results = compare_tree_models(data_train, data_test,\

outcome='fully_paid', class_weights=[None, 'balanced', {0:5, 1:1},{0:6, 1:1}, {0:7, 1:1}, {0:8, 1:1}])

columns=['Depth', 'class_weight', 'Train Accuracy','Train Precision', 'Val Accuracy','Val Precision']

scores_table = pd.DataFrame(results, columns=columns)

msk = scores_table['Val Precision'] >= 0.9

scores_table[msk].sort_values(by='Val Accuracy', ascending=False).head()

| Depth | class_weight | Train Accuracy | Train Precision | Val Accuracy | Val Precision | |

|---|---|---|---|---|---|---|

| 40 | 4 | {0: 5, 1: 1} | 0.530919 | 0.908322 | 0.523170 | 0.902159 |

| 59 | 4 | {0: 6, 1: 1} | 0.530919 | 0.908322 | 0.523170 | 0.902159 |

| 62 | 7 | {0: 6, 1: 1} | 0.538950 | 0.921664 | 0.517286 | 0.900326 |

| 78 | 4 | {0: 7, 1: 1} | 0.474292 | 0.917505 | 0.470394 | 0.914966 |

| 81 | 7 | {0: 7, 1: 1} | 0.487657 | 0.932268 | 0.465612 | 0.904842 |

| 83 | 9 | {0: 7, 1: 1} | 0.495504 | 0.954543 | 0.460280 | 0.906520 |

| 82 | 8 | {0: 7, 1: 1} | 0.482609 | 0.943900 | 0.458073 | 0.903991 |

| 79 | 5 | {0: 7, 1: 1} | 0.460804 | 0.922437 | 0.457705 | 0.917415 |

| 77 | 3 | {0: 7, 1: 1} | 0.458843 | 0.918520 | 0.455866 | 0.914423 |

| 96 | 3 | {0: 8, 1: 1} | 0.458843 | 0.918520 | 0.455866 | 0.914423 |

| 102 | 9 | {0: 8, 1: 1} | 0.486145 | 0.956453 | 0.449430 | 0.904676 |

| 101 | 8 | {0: 8, 1: 1} | 0.470062 | 0.946868 | 0.448327 | 0.908759 |

| 80 | 6 | {0: 7, 1: 1} | 0.451036 | 0.930842 | 0.445200 | 0.920203 |

| 99 | 6 | {0: 8, 1: 1} | 0.451956 | 0.931425 | 0.443545 | 0.918679 |

| 100 | 7 | {0: 8, 1: 1} | 0.463461 | 0.938127 | 0.442810 | 0.911654 |

| 97 | 4 | {0: 8, 1: 1} | 0.412556 | 0.930116 | 0.416146 | 0.939144 |

| 98 | 5 | {0: 8, 1: 1} | 0.401459 | 0.936237 | 0.405112 | 0.943955 |

| 95 | 2 | {0: 8, 1: 1} | 0.336453 | 0.940714 | 0.342221 | 0.947491 |

clean_df = pd.read_pickle('/content/gdrive/My Drive/Lending Club Project/data/Pickle/clean_df_Mon.pkl').sample(frac=.05, random_state=0)

clean_df = clean_df.drop(columns = ['issue_d', 'zip_code', 'addr_state'])

data_train, data_test = train_test_split(clean_df, test_size=.1, stratify=clean_df[outcome], random_state=99);

X_train = data_train.drop(columns=outcome)

y_train = data_train[outcome]

results = compare_tree_models(data_train, data_test,\

outcome='fully_paid', class_weights=[None, 'balanced', {0:5, 1:1},{0:6, 1:1}, {0:7, 1:1}, {0:8, 1:1}])

columns=['Depth', 'class_weight', 'Train Accuracy','Train Precision', 'Val Accuracy','Val Precision']

scores_table = pd.DataFrame(results, columns=columns)

msk = scores_table['Val Precision'] >= 0.9

scores_table[msk].sort_values(by='Val Accuracy', ascending=False).head()

| Depth | class_weight | Train Accuracy | Train Precision | Val Accuracy | Val Precision | |

|---|---|---|---|---|---|---|

| 41 | 5 | {0: 5, 1: 1} | 0.550170 | 0.905982 | 0.546157 | 0.900171 |

| 42 | 6 | {0: 5, 1: 1} | 0.549413 | 0.910787 | 0.541192 | 0.901085 |

| 62 | 7 | {0: 6, 1: 1} | 0.530613 | 0.922110 | 0.521883 | 0.900735 |

| 61 | 6 | {0: 6, 1: 1} | 0.525259 | 0.916513 | 0.520780 | 0.905317 |

| 60 | 5 | {0: 6, 1: 1} | 0.519434 | 0.912385 | 0.516182 | 0.905732 |

from sklearn.pipeline import make_pipeline

from sklearn.preprocessing import PolynomialFeatures

X_train = data_train.drop(columns=outcome)

y_train = data_train[outcome]

X_val = data_test.drop(columns=outcome)

y_val = data_test[outcome]

scores = []

for i in range(2,11):

print(i)

clf = make_pipeline(PolynomialFeatures(degree=2, include_bias=False),

DecisionTreeClassifier(criterion='gini', max_depth=i,

class_weight={0:5, 1:1}))

clf.fit(X_train, y_train)

y_train_pred = clf.predict(X_train)

y_val_pred = clf.predict(X_val)

train_accuracy = accuracy_score(y_train, y_train_pred)

train_balanced_accuracy = balanced_accuracy_score(y_train, y_train_pred)

train_precision = precision_score(y_train, y_train_pred)

train_cm = confusion_matrix(y_train, y_train_pred)

val_accuracy = accuracy_score(y_val, y_val_pred)

val_balanced_accuracy = balanced_accuracy_score(y_val, y_val_pred)

val_precision = precision_score(y_val, y_val_pred)

val_cm = confusion_matrix(y_val, y_val_pred)

scores.append({'Depth': i,

'Train Accuracy': train_accuracy,

'Train Balanced Accuracy': train_balanced_accuracy,

'Train Precision': train_precision,

'Val Accuracy': val_accuracy,

'Val Balanced Accuracy': val_balanced_accuracy,

'Val Precision': val_precision,})

clear_output()

columns=['Depth', 'Train Accuracy','Train Precision', 'Val Accuracy','Val Precision']

scores_table = pd.DataFrame(scores, columns=columns)

msk = scores_table['Val Precision'] >= 0.9

scores_table[msk].sort_values(by='Val Accuracy', ascending=False).head()

| Depth | Train Accuracy | Train Precision | Val Accuracy | Val Precision |

|---|

scores_table.sort_values(by='Val Precision', ascending=False).head()

| Depth | Train Accuracy | Train Precision | Val Accuracy | Val Precision | |

|---|---|---|---|---|---|

| 0 | 2 | 0.520517 | 0.905729 | 0.514160 | 0.899906 |

| 1 | 3 | 0.520517 | 0.905729 | 0.514160 | 0.899906 |

| 4 | 6 | 0.590060 | 0.907898 | 0.584038 | 0.894917 |

| 3 | 5 | 0.579168 | 0.903548 | 0.574476 | 0.894328 |

| 5 | 7 | 0.604753 | 0.911508 | 0.587900 | 0.890167 |

Decision Tree Model Tuning/Comparison

clean_df = pd.read_pickle('/content/gdrive/My Drive/Lending Club Project/data/Pickle/clean_df_Mon.pkl').sample(frac=.05, random_state=0)

outcome='fully_paid'

data_train, data_test = train_test_split(clean_df, test_size=.1, stratify=clean_df[outcome], random_state=99);

print(data_train.shape, data_test.shape)

data_train, data_val = train_test_split(data_train, test_size=.2, stratify=data_train[outcome], random_state=99)

print(data_train.shape, data_val.shape)

X_train = data_train.drop(columns=['issue_d', 'zip_code', 'addr_state', outcome])

y_train = data_train[outcome]

importances = ['int_rate', 'sub_grade', 'dti', 'installment', 'avg_cur_bal', 'mo_sin_old_rev_tl_op', 'bc_open_to_buy', 'credit_line_age', 'tot_hi_cred_lim', 'annual_inc', 'revol_util', 'bc_util', 'mo_sin_old_il_acct', 'revol_bal', 'total_rev_hi_lim', 'total_bc_limit', 'tot_cur_bal', 'total_bal_ex_mort', 'loan_amnt', 'total_il_high_credit_limit', 'mths_since_recent_bc', 'total_acc', 'mo_sin_rcnt_rev_tl_op', 'num_rev_accts', 'num_il_tl', 'grade', 'mths_since_recent_inq', 'mo_sin_rcnt_tl', 'num_bc_tl', 'acc_open_past_24mths', 'open_acc', 'num_sats', 'pct_tl_nvr_dlq', 'num_op_rev_tl', 'mths_since_last_delinq', 'percent_bc_gt_75', 'term_ 60 months', 'num_actv_rev_tl', 'num_rev_tl_bal_gt_0', 'num_bc_sats', 'num_actv_bc_tl', 'num_tl_op_past_12m', 'mths_since_recent_revol_delinq', 'mort_acc', 'mths_since_last_major_derog', 'mths_since_recent_bc_dlq', 'tot_coll_amt', 'mths_since_last_record', 'inq_last_6mths', 'num_accts_ever_120_pd', 'delinq_2yrs', 'pub_rec', 'verification_status_Verified', 'verification_status_Source Verified', 'emp_length_10+ years', 'purpose_debt_consolidation', 'emp_length_5-9 years', 'emp_length_2-4 years', 'home_ownership_RENT', 'purpose_credit_card', 'pub_rec_bankruptcies', 'home_ownership_MORTGAGE', 'home_ownership_OWN', 'num_tl_90g_dpd_24m', 'tax_liens', 'purpose_other', 'purpose_home_improvement', 'collections_12_mths_ex_med', 'purpose_major_purchase', 'purpose_small_business', 'purpose_medical', 'application_type_Joint App', 'purpose_moving', 'chargeoff_within_12_mths', 'purpose_vacation', 'delinq_amnt', 'purpose_house', 'acc_now_delinq', 'purpose_renewable_energy', 'purpose_wedding', 'home_ownership_OTHER', 'home_ownership_NONE', 'purpose_educational']

(48934, 87) (5438, 87)

(39147, 87) (9787, 87)

scores = []

features = []

for column in importances:

features.append(column)

print(features)

clear_output()

print(features)

print(len(features))

X_train = data_train[features]

y_train = data_train[outcome]

X_val = data_val[features]

y_val = data_val[outcome]

X_test = data_test[features]

y_test = data_test[outcome]

for depth in range(3,10):

for weight in range (3, 8):

rf_tmp = DecisionTreeClassifier(max_depth=depth, class_weight={0:weight, 1:1}).fit(X_train, y_train)

y_train_pred = rf_tmp.predict(X_train)

y_val_pred = rf_tmp.predict(X_val)

y_test_pred = rf_tmp.predict(X_test)

train_accuracy = accuracy_score(y_train, y_train_pred)

train_balanced_accuracy = balanced_accuracy_score(y_train, y_train_pred)

train_precision = precision_score(y_train, y_train_pred)

test_accuracy = accuracy_score(y_test,y_test_pred)

test_balanced_accuracy = balanced_accuracy_score(y_test,y_test_pred)

test_precision = precision_score(y_test,y_test_pred)

val_accuracy = accuracy_score(y_val,y_val_pred)

val_balanced_accuracy = balanced_accuracy_score(y_val,y_val_pred)

val_precision = precision_score(y_val,y_val_pred)

tn, fp, fn, tp = confusion_matrix(y_train, y_train_pred).ravel()

train_approved = tp

tn, fp, fn, tp = confusion_matrix(y_test,y_test_pred).ravel()

test_approved = tp

tn, fp, fn, tp = confusion_matrix(y_val,y_val_pred).ravel()

val_approved = tp

scores.append({'Top_N_Features': len(features),

'Depth': depth,

'Weight': rf_tmp.get_params()['class_weight'],

'Test Accuracy': test_accuracy,

'Test Balanced Accuracy': test_balanced_accuracy,

'Test Precision': test_precision,

'Test Fully Paid Loans': test_approved,

'Val Accuracy': val_accuracy,

'Val Balanced Accuracy': val_balanced_accuracy,

'Val Precision': val_precision,

'Val Fully Paid Loans': val_approved,

'Train Accuracy': train_accuracy,

'Train Balanced Accuracy': train_balanced_accuracy,

'Train Precision': train_precision,

'Train Fully Paid Loans': train_approved,

})

table_col_names = ['Top_N_Features','Depth','Weight', 'Test Accuracy', 'Test Balanced Accuracy','Test Precision','Test Fully Paid Loans',

'Val Accuracy','Val Balanced Accuracy','Val Precision','Val Fully Paid Loans','Train Accuracy','Train Balanced Accuracy',

'Train Precision','Train Fully Paid Loans']

tree_scores = pd.DataFrame(scores)

tree_scores = tree_scores[table_col_names]

path = '/content/gdrive/My Drive/Lending Club Project/data/Victor/'

#tree_scores.to_csv(path+'tree_scores.csv',index=False)

tree_scores = pd.read_csv(path+'tree_scores.csv')

tree_scores[(tree_scores['Val Precision']>=0.9)&(tree_scores['Test Precision']>=0.9)].sort_values('Val Fully Paid Loans',ascending=False).head()

| Top_N_Features | Depth | Weight | Test Accuracy | Test Balanced Accuracy | Test Precision | Test Fully Paid Loans | Val Accuracy | Val Balanced Accuracy | Val Precision | Val Fully Paid Loans | Train Accuracy | Train Balanced Accuracy | Train Precision | Train Fully Paid Loans | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 467 | 14 | 5 | {0: 5, 1: 1} | 0.533468 | 0.631052 | 0.90031 | 2032 | 0.538469 | 0.634381 | 0.901655 | 3704 | 0.541344 | 0.641536 | 0.907904 | 14817 |

| 432 | 13 | 5 | {0: 5, 1: 1} | 0.533468 | 0.631052 | 0.90031 | 2032 | 0.538469 | 0.634381 | 0.901655 | 3704 | 0.541344 | 0.641536 | 0.907904 | 14817 |

| 572 | 17 | 5 | {0: 5, 1: 1} | 0.533468 | 0.631052 | 0.90031 | 2032 | 0.538469 | 0.634381 | 0.901655 | 3704 | 0.541344 | 0.641536 | 0.907904 | 14817 |

| 502 | 15 | 5 | {0: 5, 1: 1} | 0.533468 | 0.631052 | 0.90031 | 2032 | 0.538469 | 0.634381 | 0.901655 | 3704 | 0.541344 | 0.641536 | 0.907904 | 14817 |

| 607 | 18 | 5 | {0: 5, 1: 1} | 0.533468 | 0.631052 | 0.90031 | 2032 | 0.538469 | 0.634381 | 0.901655 | 3704 | 0.541344 | 0.641536 | 0.907904 | 14817 |

Random Forest Model Tuning/Comparison

rf_scores = []

features = []

for column in importances[:20]:

features.append(column)

clear_output()

#print(len(features))

print(features)

X_train = data_train[features]

print(X_train.shape)

y_train = data_train[outcome]

X_val = data_val[features]

y_val = data_val[outcome]

X_test = data_test[features]

y_test = data_test[outcome]

for depth in range(3,10):

for weight in range (3, 8):

#rf_tmp = DecisionTreeClassifier(max_depth=depth, class_weight={0:weight, 1:1}).fit(X_train, y_train)

rf_tmp = RandomForestClassifier(n_estimators=20, max_depth=depth, class_weight={0:weight, 1:1}).fit(X_train, y_train)

print(X_train.shape, X_train.columns)

y_train_pred = rf_tmp.predict(X_train)

y_val_pred = rf_tmp.predict(X_val)

y_test_pred = rf_tmp.predict(X_test)

train_accuracy = accuracy_score(y_train, y_train_pred)

train_balanced_accuracy = balanced_accuracy_score(y_train, y_train_pred)

train_precision = precision_score(y_train, y_train_pred)

test_accuracy = accuracy_score(y_test,y_test_pred)

test_balanced_accuracy = balanced_accuracy_score(y_test,y_test_pred)

test_precision = precision_score(y_test,y_test_pred)

val_accuracy = accuracy_score(y_val,y_val_pred)

val_balanced_accuracy = balanced_accuracy_score(y_val,y_val_pred)

val_precision = precision_score(y_val,y_val_pred)

tn, fp, fn, tp = confusion_matrix(y_train, y_train_pred).ravel()

train_approved = tp

tn, fp, fn, tp = confusion_matrix(y_test,y_test_pred).ravel()

test_approved = tp

tn, fp, fn, tp = confusion_matrix(y_val,y_val_pred).ravel()

val_approved = tp

rf_scores.append({'Top_N_Features': len(features),

'Depth': depth,

'Weight': rf_tmp.get_params()['class_weight'],

'Test Accuracy': test_accuracy,

'Test Balanced Accuracy': test_balanced_accuracy,

'Test Precision': test_precision,

'Test Fully Paid Loans': test_approved,

'Val Accuracy': val_accuracy,

'Val Balanced Accuracy': val_balanced_accuracy,

'Val Precision': val_precision,

'Val Fully Paid Loans': val_approved,

'Train Accuracy': train_accuracy,

'Train Balanced Accuracy': train_balanced_accuracy,

'Train Precision': train_precision,

'Train Fully Paid Loans': train_approved,

})

table_col_names = ['Top_N_Features','Depth','Weight', 'Test Accuracy', 'Test Balanced Accuracy','Test Precision','Test Fully Paid Loans',

'Val Accuracy','Val Balanced Accuracy','Val Precision','Val Fully Paid Loans','Train Accuracy','Train Balanced Accuracy',

'Train Precision','Train Fully Paid Loans']

rf_scores = pd.DataFrame(rf_scores)

rf_scores = rf_scores[table_col_names]

path = '/content/gdrive/My Drive/Lending Club Project/data/Victor/'

#rf_scores.to_csv(path+'rf_scores.csv',index=False)

rf_scores = pd.read_csv(path+'rf_scores.csv')

rf_scores[(rf_scores['Val Precision']>=0.9)&(rf_scores['Test Precision']>=0.9)].sort_values('Val Fully Paid Loans',ascending=False).head()

| Top_N_Features | Depth | Weight | Test Accuracy | Test Balanced Accuracy | Test Precision | Test Fully Paid Loans | Val Accuracy | Val Balanced Accuracy | Val Precision | Val Fully Paid Loans | Train Accuracy | Train Balanced Accuracy | Train Precision | Train Fully Paid Loans | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1498 | 43 | 8 | {0: 6, 1: 1} | 0.549834 | 0.637193 | 0.900000 | 2133 | 0.553387 | 0.638784 | 0.900139 | 3876 | 0.577081 | 0.679289 | 0.930936 | 15892 |

| 1307 | 38 | 5 | {0: 5, 1: 1} | 0.548915 | 0.636959 | 0.900127 | 2127 | 0.552978 | 0.639478 | 0.900979 | 3867 | 0.557616 | 0.647306 | 0.906901 | 15547 |

| 1323 | 38 | 8 | {0: 6, 1: 1} | 0.548547 | 0.638097 | 0.901402 | 2121 | 0.552774 | 0.639350 | 0.900932 | 3865 | 0.578461 | 0.681102 | 0.932163 | 15926 |

| 588 | 17 | 8 | {0: 6, 1: 1} | 0.548731 | 0.637870 | 0.901104 | 2123 | 0.551957 | 0.639218 | 0.901122 | 3855 | 0.570925 | 0.675008 | 0.929487 | 15660 |

| 1638 | 47 | 8 | {0: 6, 1: 1} | 0.549283 | 0.638557 | 0.901570 | 2125 | 0.552570 | 0.641310 | 0.902954 | 3852 | 0.577362 | 0.681269 | 0.932906 | 15865 |

Comparison of Top Decision Tree vs. Top Random Forest Models

clean_df = pd.read_pickle('/content/gdrive/My Drive/Lending Club Project/data/Pickle/clean_df_Mon.pkl')

print('Total Number of Rows:', '{:,}'.format(clean_df.shape[0]))

print('Total Number of Columns:', '{:,}'.format(clean_df.shape[1]))

Total Number of Rows: 1,087,436

Total Number of Columns: 87

outcome='fully_paid'

data_train, data_test = train_test_split(clean_df, test_size=.1, stratify=clean_df[outcome], random_state=99);

print(data_train.shape, data_test.shape)

data_train, data_val = train_test_split(data_train, test_size=.2, stratify=data_train[outcome], random_state=99)

print(data_train.shape, data_val.shape)

(978692, 87) (108744, 87)

(782953, 87) (195739, 87)

importances = ['int_rate', 'sub_grade', 'dti', 'installment', 'avg_cur_bal', 'mo_sin_old_rev_tl_op', 'bc_open_to_buy', 'credit_line_age', 'tot_hi_cred_lim', 'annual_inc', 'revol_util', 'bc_util', 'mo_sin_old_il_acct', 'revol_bal', 'total_rev_hi_lim', 'total_bc_limit', 'tot_cur_bal', 'total_bal_ex_mort', 'loan_amnt', 'total_il_high_credit_limit', 'mths_since_recent_bc', 'total_acc', 'mo_sin_rcnt_rev_tl_op', 'num_rev_accts', 'num_il_tl', 'grade', 'mths_since_recent_inq', 'mo_sin_rcnt_tl', 'num_bc_tl', 'acc_open_past_24mths', 'open_acc', 'num_sats', 'pct_tl_nvr_dlq', 'num_op_rev_tl', 'mths_since_last_delinq', 'percent_bc_gt_75', 'term_ 60 months', 'num_actv_rev_tl', 'num_rev_tl_bal_gt_0', 'num_bc_sats', 'num_actv_bc_tl', 'num_tl_op_past_12m', 'mths_since_recent_revol_delinq', 'mort_acc', 'mths_since_last_major_derog', 'mths_since_recent_bc_dlq', 'tot_coll_amt', 'mths_since_last_record', 'inq_last_6mths', 'num_accts_ever_120_pd', 'delinq_2yrs', 'pub_rec', 'verification_status_Verified', 'verification_status_Source Verified', 'emp_length_10+ years', 'purpose_debt_consolidation', 'emp_length_5-9 years', 'emp_length_2-4 years', 'home_ownership_RENT', 'purpose_credit_card', 'pub_rec_bankruptcies', 'home_ownership_MORTGAGE', 'home_ownership_OWN', 'num_tl_90g_dpd_24m', 'tax_liens', 'purpose_other', 'purpose_home_improvement', 'collections_12_mths_ex_med', 'purpose_major_purchase', 'purpose_small_business', 'purpose_medical', 'application_type_Joint App', 'purpose_moving', 'chargeoff_within_12_mths', 'purpose_vacation', 'delinq_amnt', 'purpose_house', 'acc_now_delinq', 'purpose_renewable_energy', 'purpose_wedding', 'home_ownership_OTHER', 'home_ownership_NONE', 'purpose_educational']

features = importances[0:43]

depth = 8

weight = 6

X_train = data_train[features]

y_train = data_train[outcome]

X_val = data_val[features]

y_val = data_val[outcome]

X_test = data_test[features]

y_test = data_test[outcome]

rf_model = RandomForestClassifier(n_estimators=50, max_depth=depth, class_weight={0:weight, 1:1}).fit(X_train, y_train)

rf_model = RandomForestClassifier(n_estimators=50, max_depth=8, class_weight={0:6, 1:1}).fit(X_train, y_train)

data_test['RF_Model_Prediction'] = rf_model.predict(X_test)

data_test['RF_Probability_Fully_Paid'] = rf_model.predict_proba(X_test)[:,1]

features = importances[0:13]

depth = 5

weight = 5

X_train = data_train[features]

y_train = data_train[outcome]

X_val = data_val[features]

y_val = data_val[outcome]

X_test = data_test[features]

y_test = data_test[outcome]

rf_model = DecisionTreeClassifier(max_depth=depth, class_weight={0:weight, 1:1}).fit(X_train, y_train)

data_test['Tree_Model_Prediction'] = rf_model.predict(X_test)

data_test['Tree_Probability_Fully_Paid'] = rf_model.predict_proba(X_test)[:,1]

data_test[['RF_Model_Prediction','Tree_Model_Prediction','RF_Probability_Fully_Paid','Tree_Probability_Fully_Paid']].describe()

| RF_Model_Prediction | Tree_Model_Prediction | RF_Probability_Fully_Paid | Tree_Probability_Fully_Paid | |

|---|---|---|---|---|

| count | 108744.000000 | 108744.000000 | 108744.000000 | 108744.000000 |

| mean | 0.366908 | 0.436806 | 0.447268 | 0.484344 |

| std | 0.481963 | 0.495993 | 0.167528 | 0.178238 |

| min | 0.000000 | 0.000000 | 0.124550 | 0.187470 |

| 25% | 0.000000 | 0.000000 | 0.318232 | 0.357840 |

| 50% | 0.000000 | 0.000000 | 0.421940 | 0.455652 |

| 75% | 1.000000 | 1.000000 | 0.563963 | 0.616304 |

| max | 1.000000 | 1.000000 | 0.888068 | 0.864915 |

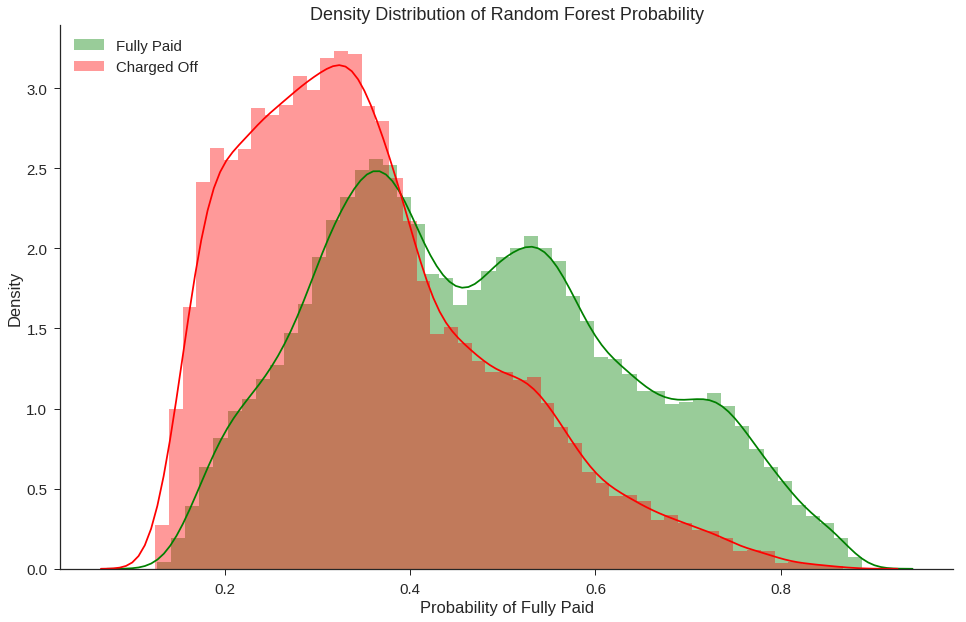

With similar total funded fully paid loans between the best Decision Tree and Random Forest, we need to look at the probability distributions. Because it is unrealistic to expect investors to invest in all loans we recommend, we will rank the loans by order of probability. As such, the performance of the models at predicting loans near 1.0 matters more than the loans near 0.5 as those will be fulfilled first.

fig, ax = plt.subplots(figsize=(16,10))

sns.distplot(data_test[data_test['fully_paid']==1]['RF_Probability_Fully_Paid'],color='green',rug=False,label='Fully Paid')

sns.distplot(data_test[data_test['fully_paid']==0]['RF_Probability_Fully_Paid'],color='red',rug=False,label='Charged Off')

ax.set_title('Density Distribution of Random Forest Probability')

ax.set_xlabel('Probability of Fully Paid')

ax.set_ylabel('Density')

plt.legend(loc='upper left')

sns.despine()

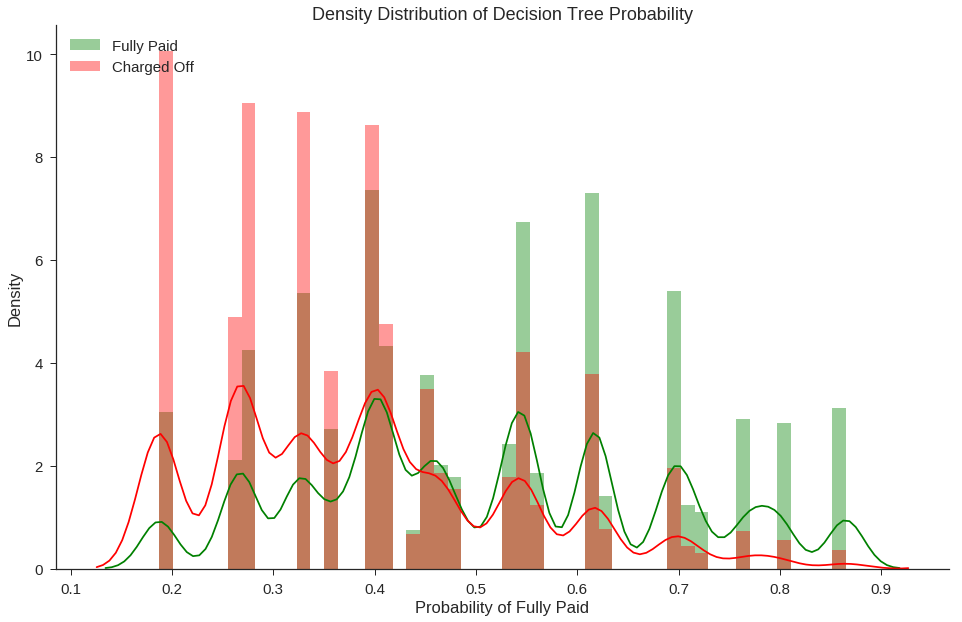

fig, ax = plt.subplots(figsize=(16,10))

sns.distplot(data_test[data_test['fully_paid']==1]['Tree_Probability_Fully_Paid'],color='green',rug=False,label='Fully Paid')

sns.distplot(data_test[data_test['fully_paid']==0]['Tree_Probability_Fully_Paid'],color='red',rug=False,label='Charged Off')

ax.set_title('Density Distribution of Decision Tree Probability')

ax.set_xlabel('Probability of Fully Paid')

ax.set_ylabel('Density')

plt.legend(loc='upper left')

sns.despine()

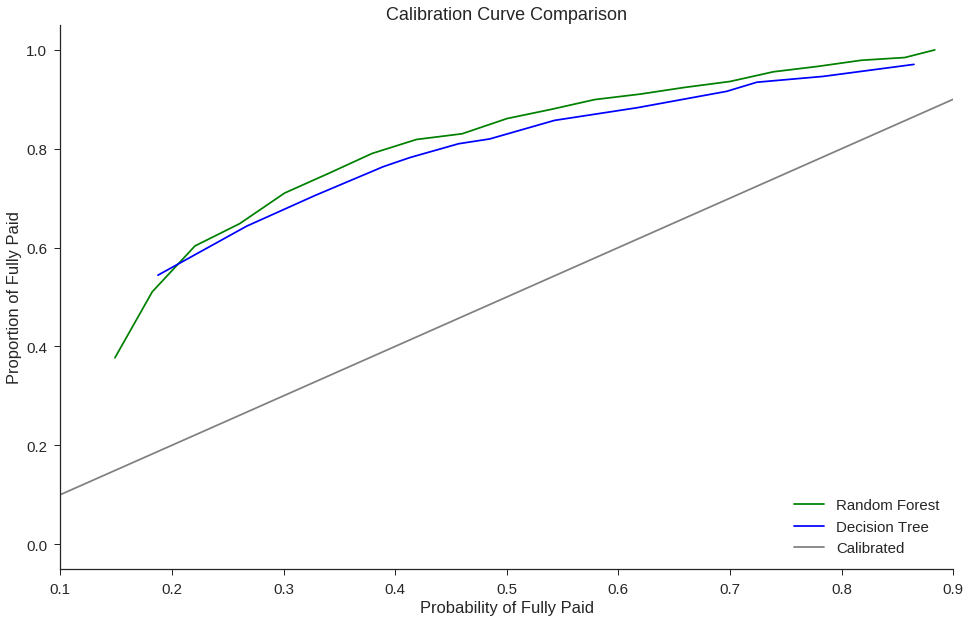

from sklearn.calibration import calibration_curve

rf_positive_frac, rf_mean_score = calibration_curve(y_test, data_test['RF_Probability_Fully_Paid'].values, n_bins=25)

tree_positive_frac, tree_mean_score = calibration_curve(y_test, data_test['Tree_Probability_Fully_Paid'].values, n_bins=25)

fig, ax = plt.subplots(figsize=(16,10))

ax.plot(rf_mean_score,rf_positive_frac, color='green', label='Random Forest')

ax.plot(tree_mean_score,tree_positive_frac, color='blue', label='Decision Tree')

ax.plot([0, 1], [0, 1], color='grey', label='Calibrated')

ax.set_title('Calibration Curve Comparison')

ax.set_xlabel('Probability of Fully Paid')

ax.set_ylabel('Proportion of Fully Paid')

ax.set_xlim([.1, .9])

plt.legend(loc='lower right')

sns.despine()

Because we chose models with a high base precision, the calibration curve is not suprising.

Our use case will only focus on the upper end of the probability scores where an approved charged off loan is the worst misclasification so it is not a big issue that the probabilities are not 1:1 to the proportion of fully paid loans. What we see is that our chosen Random Forest model has higher proportion of fully paid loans in comparison to Decision Tree at high probability values. While the Decision Tree is more interpretable, Random Forest is a good balance between performance and interpretability.